Credit Bureau Reporting Services

Employment credit reports through TransUnion and Equifax, plus tenant screening for property owners — handled with strict permissible-purpose compliance. Trusted since 1979.

Credit bureau reporting gives employers insight into a candidate’s financial responsibility for roles where money is on the line — but it’s one of the most heavily regulated screening tools available, and using it incorrectly creates real legal exposure. DDS provides credit bureau reporting through TransUnion and Equifax employment credit products, applied only to roles with a legitimate permissible purpose and always with a separate signed release on file. For positions where employees can access funds, credit bureau reporting is a prudent safeguard handled the compliant way.

TransUnion & Equifax Products

Separate Signed Release Required

Tenant Screening for Property Owners

Permissible-Purpose Compliant

What Is Credit Bureau Reporting for Employment?

Credit bureau reporting for employment is the use of consumer credit information to evaluate a candidate’s financial responsibility for positions where that responsibility is job-relevant. It is distinct from the credit reports used in lending decisions — and the distinction matters legally.

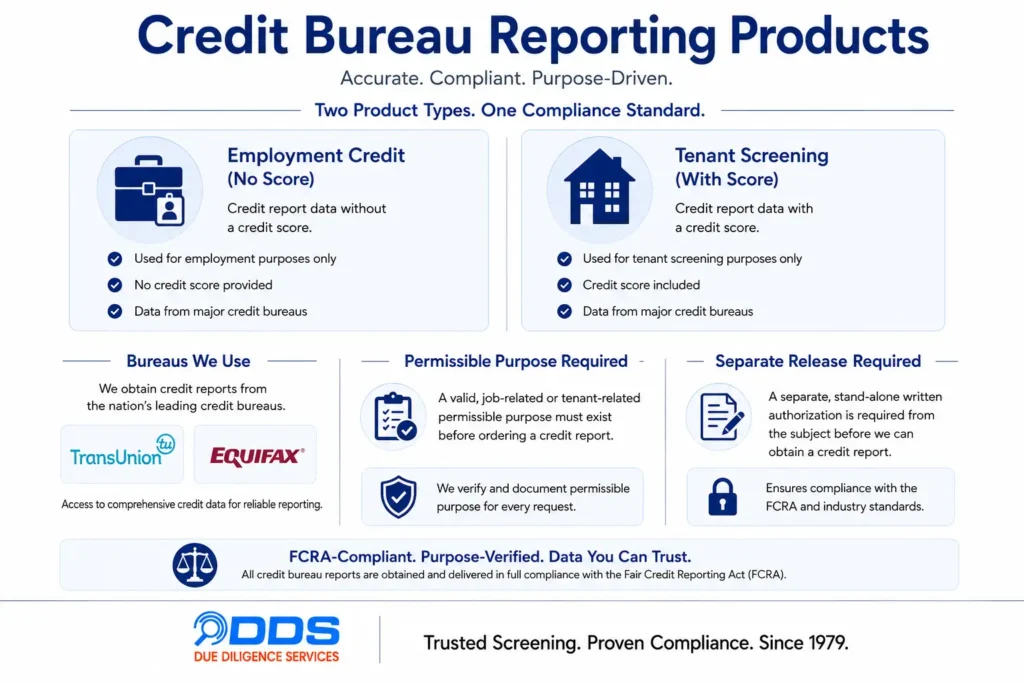

An employment credit report is a specialized product. Unlike a lending credit report, an employment credit report does not include a credit score. It shows the candidate’s credit history — accounts, payment history, public records, and similar information — but omits the score that lenders use, because a score is not appropriate for an employment decision. The purpose is to assess patterns of financial responsibility relevant to a role, not to make a lending judgment.

DDS provides credit bureau reporting using employment consumer credit products from TransUnion and Equifax. For property owners who need tenant evaluation, DDS also provides tenant screening reports — which, unlike employment reports, do include a score where appropriate for that purpose.

The Credit Products DDS Provides

DDS provides credit bureau reporting through two of the three major bureaus, using the right product for the right purpose:

Employment Consumer Credit Reports (TransUnion and Equifax). For employment screening, DDS uses employment-version consumer credit reports from TransUnion and Equifax. These reports show credit history relevant to financial responsibility without the credit score, consistent with the appropriate use of credit information in hiring.

Tenant Screening Reports (with score). For property owners evaluating prospective tenants, DDS provides tenant screening reports. Because tenant screening serves a different permissible purpose than employment, these reports include a score where appropriate — giving property owners the standardized risk indicator that’s relevant to a rental decision.

Using the correct product for each purpose isn’t just good practice — it’s a compliance requirement. The employment product and the tenant product serve different permissible purposes under the Fair Credit Reporting Act, and DDS applies the right one to each situation.

When Credit Bureau Reporting Is Appropriate

Credit bureau reporting is not appropriate for every role — and using it where it isn’t job-relevant creates legal risk. The guiding principle is straightforward: credit information should be considered only where the job genuinely involves financial responsibility.

Credit bureau reporting is most commonly and legitimately used for roles where employees can access funds — especially cash. Examples include:

– Cash-handling positions — retail cash management, banking, cashiers with significant register responsibility

– Financial roles — accounting, bookkeeping, payroll, accounts payable/receivable

– Fiduciary positions — anyone managing or with access to company or client funds

– Executive and signing authority — leadership roles with financial control

– Roles with financial-system access — positions that can initiate or approve transactions

Wherever monetary funds can be accessed — and especially where cash is involved — credit bureau reporting is a prudent and defensible screening step. For roles without financial responsibility, it generally isn’t appropriate, and DDS will advise accordingly.

Not sure if credit reporting applies to your roles?

Compliance and Permissible PurposeA 20-minute consultation will help you determine which positions justify credit bureau reporting under permissible-purpose rules — and which don’t. Getting this right protects your organization from compliance exposure. No obligation, no charge.

Compliance and Permissible Purpose

Credit bureau reporting is among the most regulated tools in employment screening. The Fair Credit Reporting Act, plus a growing patchwork of state and local laws, governs when an employer may pull credit information and how it must be handled.

DDS applies strict compliance controls to all credit bureau reporting:

Separate signed release for permissible purpose. Credit bureau reporting requires its own separate signed release form — distinct from the general background check authorization. The candidate must specifically authorize the credit pull, establishing the permissible purpose required under the FCRA. DDS requires this separate release on file before any credit report is pulled.

Job-relevance standard. Most state and local restrictions on employment credit checks turn on the job title and its responsibilities. The restrictions generally permit credit checks for positions involving financial interaction or access to funds, while limiting them for roles where credit has no bearing. DDS applies credit bureau reporting consistent with the role’s responsibilities and the applicable jurisdictional rules.

Evolving regulatory compliance. Because state and city rules on employment credit checks continue to change, DDS keeps its credit bureau reporting practices current with the evolving regulatory landscape.

This compliance discipline protects the employer. A credit check pulled without proper permissible purpose, separate authorization, or job-relevance can expose an organization to FCRA litigation and state-law penalties. DDS structures credit bureau reporting to avoid that exposure.

Why Employers Choose DDS for Credit Bureau Reporting

1. The right product for the purpose. Employment consumer credit reports for hiring (no score), tenant screening reports for property owners (with score) — DDS applies the correct product to each permissible purpose.

2. TransUnion and Equifax. DDS provides credit bureau reporting through established major-bureau consumer credit products.

3. Separate signed release enforced. DDS requires a separate signed release establishing permissible purpose before any credit report is pulled — no shortcuts on authorization.

4. Job-relevance discipline. DDS applies credit bureau reporting only where the role’s financial responsibilities justify it, consistent with state and local restrictions.

5. Evolving compliance. As state and city rules on employment credit checks change, DDS keeps its practices current.

6. Role-appropriate guidance. DDS advises which roles legitimately warrant credit reporting and which don’t — protecting clients from over-applying a heavily regulated tool.

7. Operating since 1979. Decades of experience handling credit information for employment within the bounds of the FCRA and evolving state law.

Frequently Asked Questions

Which credit bureaus does DDS use?

DDS provides credit bureau reporting through TransUnion and Equifax consumer credit products. For employment screening, DDS uses employment-version consumer credit reports; for property owners, DDS provides tenant screening reports.

Do employment credit reports include a credit score?

No. Employment consumer credit reports do not include a credit score. They show credit history relevant to financial responsibility — accounts, payment history, and public records — without the score lenders use, because a score is not appropriate for an employment decision. Tenant screening reports for property owners do include a score, since that serves a different permissible purpose.

What's the difference between an employment credit report and a lending credit report?

A lending credit report includes a credit score and is used to make lending decisions. An employment credit report omits the score and is used to assess patterns of financial responsibility relevant to a job. They are different products serving different permissible purposes under the FCRA. DDS uses the employment product for hiring.

Which roles can legitimately have a credit check?

Credit bureau reporting is appropriate for roles where employees can access funds — especially cash. This includes cash-handling positions, financial and accounting roles, fiduciary positions, executive and signing authority, and roles with financial-system access. Wherever monetary funds can be accessed, a credit check is a defensible step. For roles without financial responsibility, it generally isn’t appropriate.

Do state laws restrict employment credit checks?

Yes. Many states and cities restrict or limit employment credit checks, and most restrictions turn on the job title and its responsibilities — generally permitting credit checks for positions involving financial interaction or access to funds while limiting them otherwise. DDS applies credit bureau reporting consistent with the role’s responsibilities and applicable jurisdictional rules, and keeps its practices current as those rules evolve.

What authorization is required for a credit check?

Credit bureau reporting requires a separate signed release form, distinct from the general background check authorization. The candidate must specifically authorize the credit pull, establishing the permissible purpose the FCRA requires. DDS requires this separate signed release on file before any credit report is pulled.

Does DDS offer tenant screening?

Yes. For property owners, DDS provides tenant screening reports through its credit bureau reporting service. Unlike employment credit reports, tenant screening reports include a score where appropriate, giving property owners a standardized risk indicator relevant to a rental decision.

How does DDS keep credit reporting compliant?

DDS uses the correct product for each permissible purpose, requires a separate signed release before pulling credit, applies credit reporting only where the role’s financial responsibilities justify it, and keeps its practices current with evolving state and local rules. This compliance discipline protects the employer from FCRA and state-law exposure.

Ready to Add Compliant Credit Reporting to Your Program?

A free consultation shows you how credit bureau reporting fits your screening program — which roles justify it, which products apply, and how DDS keeps it permissible-purpose compliant. No obligation, no charge.